December 16, 2020

Worried About Your Retirement Savings?

Retirement can be scary for any number of reasons. One widespread fear is running out of money: nearly 50% of Americans named this as their number one retirement concern.

It’s not irrational to worry about outspending your savings, especially as life expectancy increases and healthcare grows more and more expensive. However, some simple rules of thumb and smart investment decisions can take some of the uncertainty out of retirement planning.

How much money do you need to retire?

There is no “one size fits all'' number for retirement planning. The amount of money you’ll need to save is highly personal and dependent on a number of factors. Some things, such as how long you’ll live or what you’ll spend on medical care, are mostly outside of your control. However, you can influence some factors, such as your age of retirement or the lifestyle you would like to maintain.

In general, the AARP estimates that retirees will need around 80% of their annual pre-retirement income to maintain a comfortable lifestyle. This estimate takes into account the fact that retirees will no longer have certain expenses such as 401k contributions, payroll taxes, or other costs associated with going to work every day.

This 80% number takes into account all sources of income. The amount you’ll need to draw from your savings will be offset by other sources of income you’ll have in retirement, such as social security, annuity income or passive income from investments like real estate or farmland. The greater your income from other sources, the less you’ll have to draw down on your nest egg. For example, if you’ll need $5,000 a month in retirement and you have $2,000 from other sources, you will only need to pull $3,000 a month from your retirement savings.

Keep in mind that 80% is only a rule of thumb, and actual annual expenses will vary significantly from person to person. Do you own your home outright, or will you still have a mortgage? Do you plan on traveling extensively once you’re no longer glued to your desk? How much debt will you still have to pay off?

Once you have an idea of the annual income you’ll need, the question becomes how much money will you need to save before you can retire. A commonly used rule of thumb is the 4% rule. This states that if you withdraw 4% of your retirement savings each year (adjusted for inflation), your savings should last for 30 years of retirement. The 4% rule can be used to calculate total retirement savings -- just multiply your expected annual cost of living by 25. For example, if you plan on living on $40,000 a year, you should target $1 million in savings by the time you retire.

Save early and save often

This may seem like a daunting sum. Fortunately, investors have a powerful tool on their side: compound interest.

Compound interest means that as your investments generate returns; these returns are reinvested and your money earns more money. The more time you give your investments to compound, the larger your retirement savings will be when you’re ready to leave the workforce. The magic of compound interest means that even if you can only save a little at a time, you should start saving as early as possible.

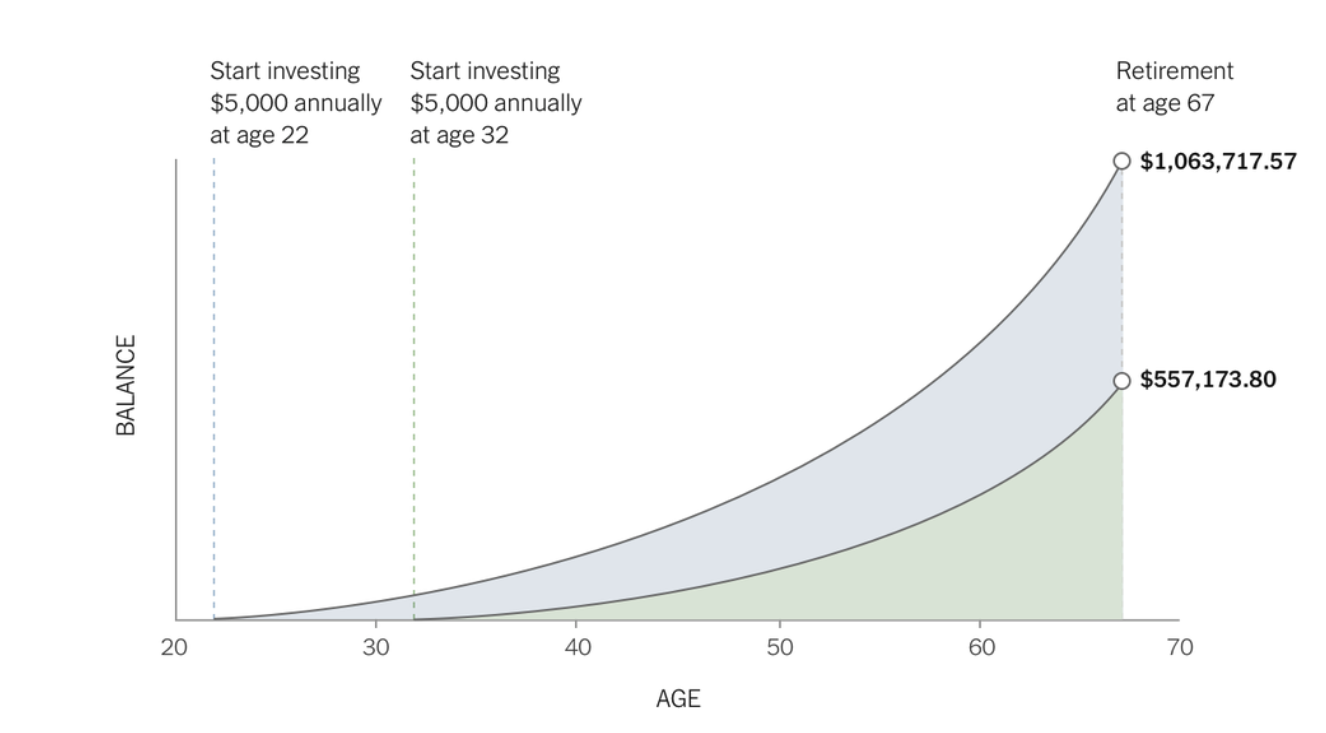

In the example below, one investor starts saving $5,000 each year from age 22 to age 67, and a second investor saves the same amount each year but doesn’t start until age 32. Both investors receive an annual return of 6% (well below the average annual returns of the stock market). As you can see from the chart below, the first investor saves only $50,000 more than the second investor but has nearly twice the amount saved at retirement — all through compounding.

Finding the right investment mix for your retirement savings

Once you’ve started saving for retirement, it’s essential to find the right mix of assets for your retirement savings. First, it’s important to keep in mind your risk tolerance and investment horizon. If you’re planning on retiring in 20 or 30 years, your portfolio mix will look very different compared to someone who is planning on retiring in the next five years. Most experts recommend that investors should consider a riskier/more aggressive asset allocation further away from retirement and shift towards a less risky/more conservative asset allocation as they get closer to retirement.

If you are many decades away from retirement, it may be tempting to put as much money as possible into stocks, as these returns are much more attractive than bonds or cash. However, diversification is extremely important for building wealth. A diverse portfolio made up of multiple uncorrelated asset classes is much less volatile. Volatility can significantly reduce your returns over the long term, making it especially dangerous for your retirement savings.

Another factor to consider with retirement savings is the more diversity you have, the less likely that you’ll be forced to sell an investment at a loss. You have no control over the performance of the market. If 100% of your savings are invested in stocks and the market collapses after you’re retired, you would be in the painful position of having to sell anyway and lock in your losses. This would be bad news for your savings long-term. Instead, it’s better to have a mix of lower-risk and higher-risk investments in your retirement portfolio.

Where alternative investments fit into your retirement portfolio

When investing for retirement, most people consider allocating their funds between a mix of traditional investments like stocks and bonds. However, there is a broad universe of alternative investments that can offer a strong complement to an existing retirement portfolio.

Alternative investments (or “alternatives”) include any non-traditional investments, including private equity, commodities such as gold, real estate, or farmland. Alternatives offer investors several benefits. First, they are uncorrelated with public markets, meaning that adding alternatives to a portfolio increases diversification. Alternatives also tend to be less volatile than the stock market. Alternatives can offer better returns than traditional investments, and some also have the benefit of providing passive income. While alternatives are not available through most traditional IRAs, they can be accessed with a self-directed IRA, which gives you more control over your savings and allows you to access a much broader range of investment opportunities.

It’s essential to choose the right mix of alternative investments for your portfolio. One asset class that offers many benefits to investors focused on saving for retirement is farmland. Farmland is a newer category of real estate for many investors which has recently become accessible thanks to FarmTogether’s technology-enabled investment platform.

Farmland has several characteristics which make it worth considering for your retirement portfolio. It is a real asset with scarcity value which has provided consistently positive returns since 1991. In that time, total annual returns have averaged ~10% (including income and price appreciation), while volatility is below that of stocks and traditional real estate. Another attractive feature for retirement investors is that farmland provides a good source of passive income, reducing your reliance on selling your savings. Finally, farmland performs well during a recession and offers an effective hedge against rising inflation, which is particularly important for long-term investments like your retirement savings.

Click here to see farmland's historical performance, visit our FAQ to learn more about investing with FarmTogether, or get started today by visiting ways to invest.

Disclaimer: FarmTogether is not a registered broker-dealer, investment advisor or investment manager. FarmTogether does not provide tax, legal or investment advice. This material has been prepared for informational and educational purposes only. You should consult your own tax, legal and investment advisors before engaging in any transaction.

Was this article helpful?