December 28, 2020

Why Volatility Can Be Bad For Long-Term Returns

As an investor, it’s hard to look at the news these days without hearing about volatility. 2020 has been a roller coaster year for a lot of reasons, not least of all because of the whiplash-inducing swings in the stock market over the past nine months.

But what do we really mean when we talk about volatility, and why is it something that long-term investors might want to avoid? Read on to find out more and learn how to protect your portfolio in these uncertain times.

What is volatility?

When we talk about volatility, we’re really talking about how much the price of an investment is likely to fluctuate. Volatility measures the degree of change in price over a period of time. High-volatility investments, like stocks, experience wide price swings in a very short period of time. In contrast, the price of low-volatility investments, like U.S. government bonds or farmland, remains relatively steady over time.

Many investors consider “volatility” as synonymous with “risk.” In this view, risk is a necessary evil in order to receive the benefits of higher returns. In fact, volatility is only one of the many risks investors face. It’s also not necessary to have a volatile portfolio in order to make an attractive return. Instead, by using a few basic principles, smart investors can enjoy the benefits of strong returns while significantly reducing their risk exposure.

Rule No. 1: Don’t lose money

For day traders, who earn their living taking risks and making bets on the market, volatility is an opportunity. For most long-term investors, though, volatility is something to be avoided whenever possible because it is a good way of losing money. While volatile investments can deliver stellar returns, they can just as easily lead to large losses. As Warren Buffet famously said about investing, “Rule No.1: Never lose money. Rule No.2: Never forget rule No.1.”

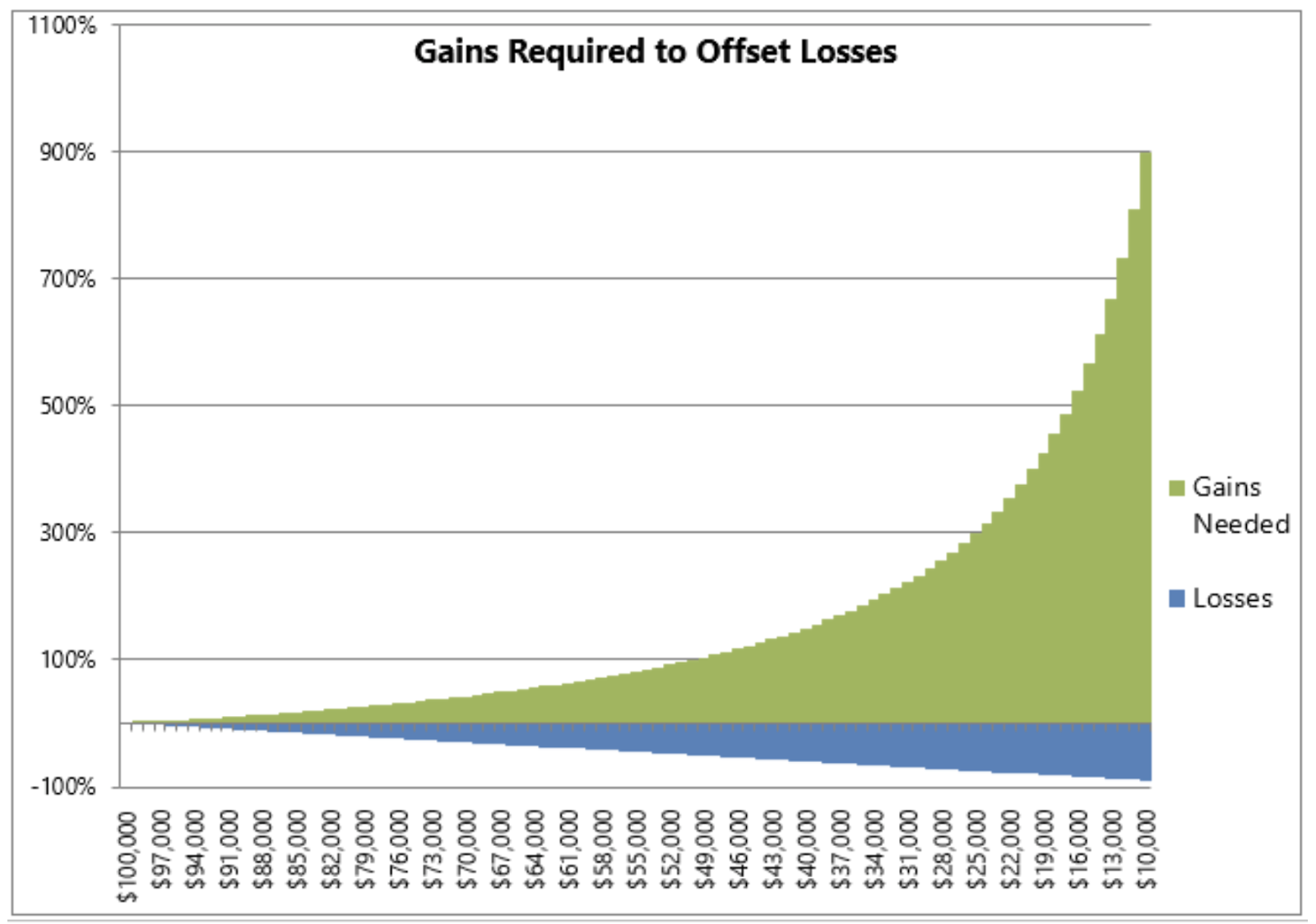

Once your portfolio loses value, it needs to achieve an even greater return just to get back to its starting point. For example, suppose you buy a stock for $100, which then decreases by 50% to $50. To return to its original value of $100, the stock price needs to increase by 100% to achieve a total return of 0%.

The chart below illustrates this on a larger scale. As losses increase, exponentially greater gains are required to get your portfolio back to where you started from.

Volatility can be destructive to wealth in the short and long term

For long-term investors, volatility can destroy wealth a couple of ways. First, volatility creates fear and uncertainty, which can lead to bad investment decisions. While investors know in theory that they should “buy low, sell high,” in periods of extreme volatility it is often the reverse. Too many investors see a big drop in the value of their portfolio and sell to avoid further losses. Panic selling like this is a mistake because it locks in your losses for the long term. Volatility can also make investors fearful about investing more money in the market, meaning they miss out on good trading days and the benefits of long-term compounding.

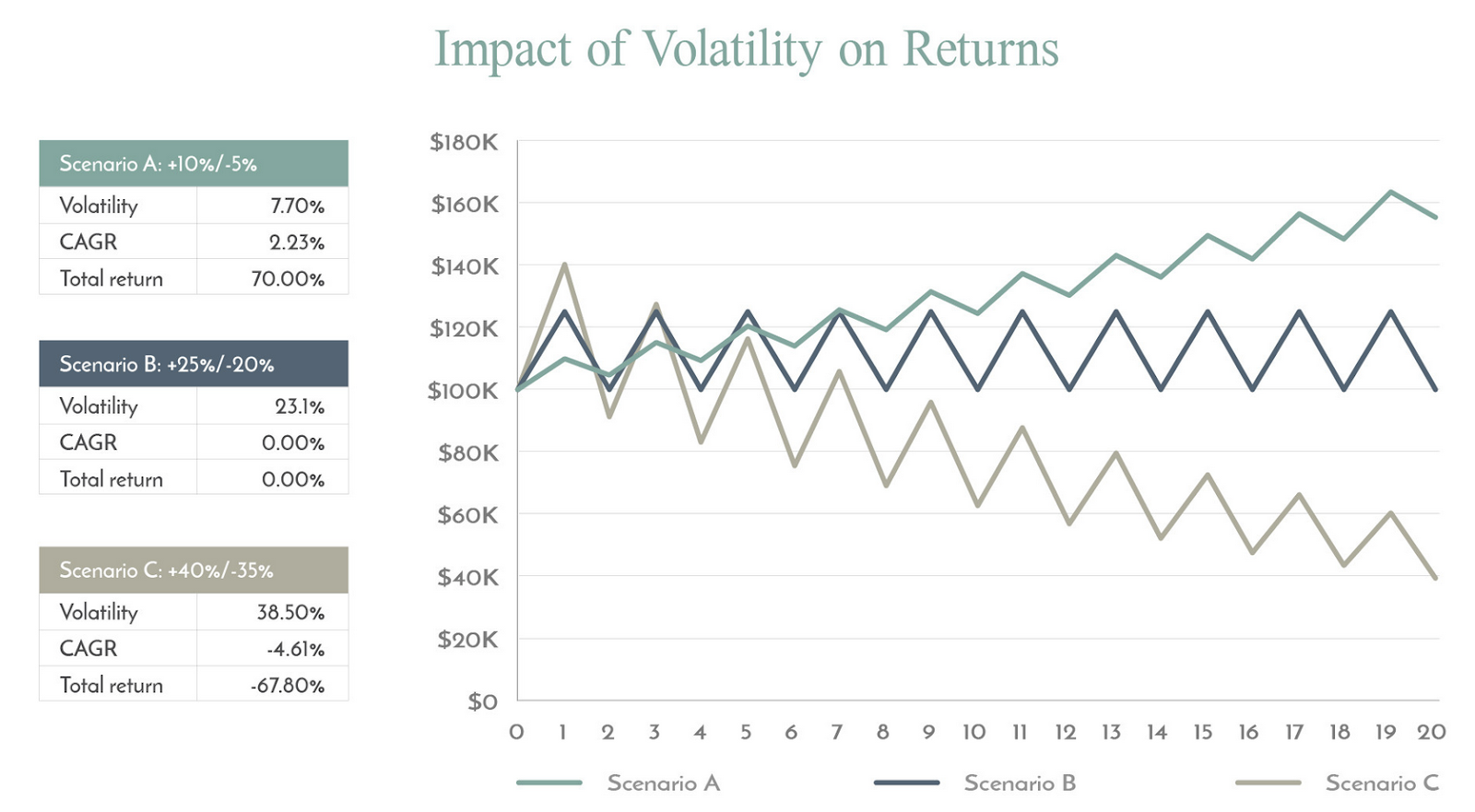

Volatility also eats into your returns long term. Although volatile portfolios are more likely to have higher returns in good years, they are also more likely to have higher losses in bad years. What this means is that, over time, your portfolio is growing from a smaller starting point. This concept — known as “volatility drag” — is crucial for understanding why volatility can be bad for your long-term wealth.

For example, take the three hypothetical portfolios below. Portfolio (Scenario) A has the lowest volatility. In any given year, it never grows by more than 10% or loses more than 5% of its value. Over a 20-year period, Portfolio A grows by 55%. In contrast, Portfolio (Scenario) C is much more volatile. It achieves higher returns of 40% but also experiences greater losses (35% compared to only 5%). The net effect in this case is that Portfolio C gradually loses value over time.

The takeaway, which may be counter-intuitive, is that it’s better to have lower returns and lower volatility than higher returns paired with higher volatility when thinking long-term.

Volatility has increased over time and is here to stay

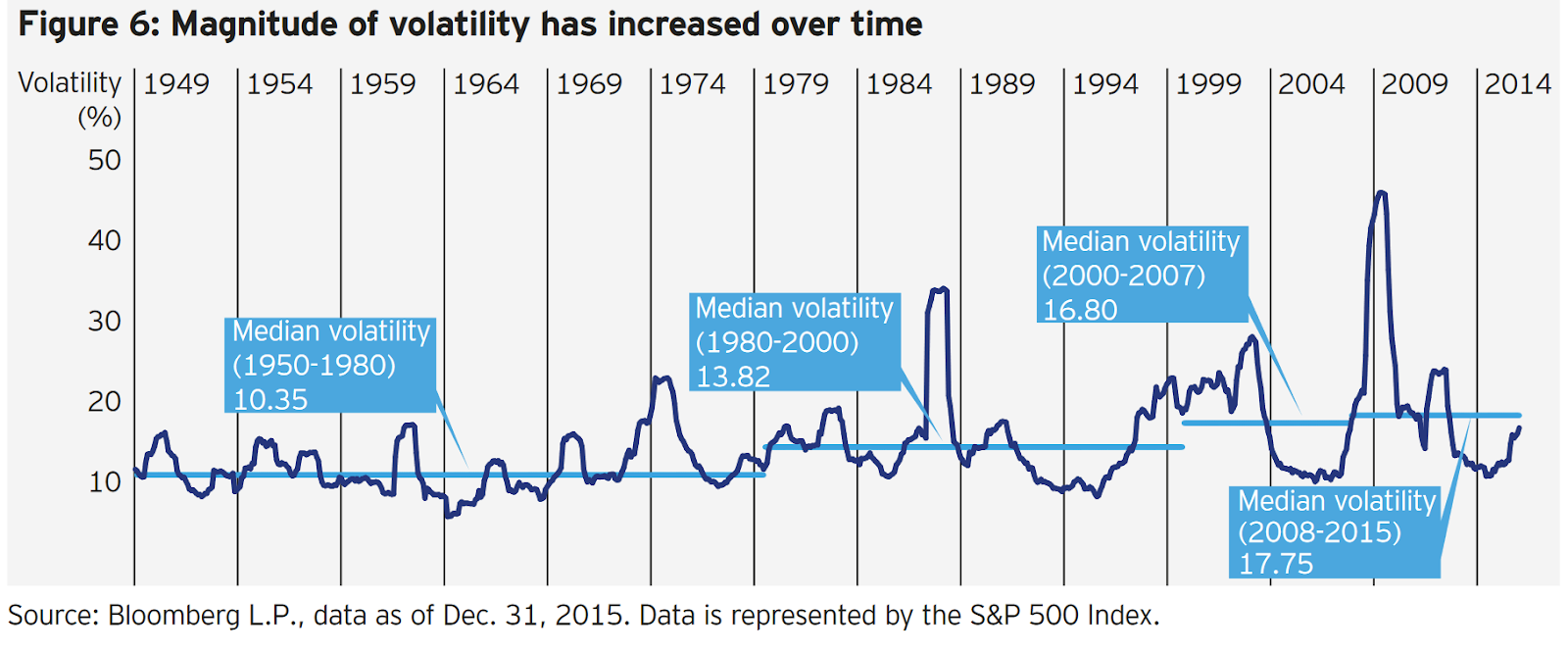

If it feels like the stock market is more volatile today than it used to be, that’s because it is.

As the chart below illustrates, the magnitude of volatility in the stock market has increased over time. In the decades between 1950 and 1980, median volatility was around 10.3%. In contrast, median volatility increased to 13.8% in 1980 - 2000 and 16.8% between 2000 and 2007. Shockingly, since the Great Financial Crisis through 2015, median volatility increased again to 17.7%.

Following this trend, COVID-19 pandemic has ushered in a new wave of record-breaking volatility across global financial markets. This volatility has been more marked among industries most sensitive to COVID containment measures, such as hotels, airlines, restaurants, and oil & gas. There is no sign of volatility going away in the near term, meaning investors need to put in place effective strategies to mitigate losses now.

How to help reduce the impact of volatility on your portfolio

The best way of mitigating volatility is to diversify your portfolio. By investing in multiple uncorrelated asset classes, investors lower the total volatility of their portfolio. This reduces volatility drag and supports the creation of long-term wealth.

Traditionally, investors have diversified their portfolios across stocks and bonds. However, these are only one part of the picture. For savvy investors, there exists a wide range of alternative investments that offer attractive returns with other benefits. The performance of most alternative investments is uncorrelated with the performance of public markets, meaning that they are unaffected by market shocks. Many alternative investments offer returns that are equal to or better than the stock market, and some offer other benefits such as passive income.

One attractive, low-volatility alternative investment to consider is farmland. As can be seen from the chart below, U.S. farmland is significantly less volatile than the stock market and comparable to 10-year U.S. Treasuries. Despite being less risky than the stock market, farmland also offers attractive returns. Historically, returns have averaged 10% including income and price appreciation.

Farmland has other benefits as well. Unlike a stock, farmland is a real asset that preserves value during a recession. During the Great Financial Crisis, U.S. farmland returned nearly 30%. Farmland also offers a hedge against inflation, with many benefits of gold without gold’s downsides. For example, unlike gold, farmland is a good source of passive income.

Click here to see farmland's historical performance, visit our FAQ to learn more about investing with FarmTogether, or get started today by visiting ways to invest.

Disclaimer: FarmTogether is not a registered broker-dealer, investment advisor or investment manager. FarmTogether does not provide tax, legal or investment advice. This material has been prepared for informational and educational purposes only. You should consult your own tax, legal and investment advisors before engaging in any transaction.

Was this article helpful?