November 04, 2020

Investing in an Ultra-Low Interest Rate Environment

Today’s ultra-low rate environment poses a special challenge for investors. With high-quality bonds currently returning next to nothing, it is increasingly difficult to find low-risk investments that also offer an attractive return. How can you balance risk and reward in your portfolio? Read on to find out.

Ultra-low rates are here to stay

Investors have been coming to terms with investing in a low interest rate environment for over ten years, although it seemed as though bond yields were finally on the rise. That changed with the COVID-19 pandemic in March, when investors flocked to the stability of bonds. Now that the Federal Reserve has announced that interest rates will stay near zero until at least 2023, investors will be navigating this ultra-low interest rate environment for the foreseeable future.

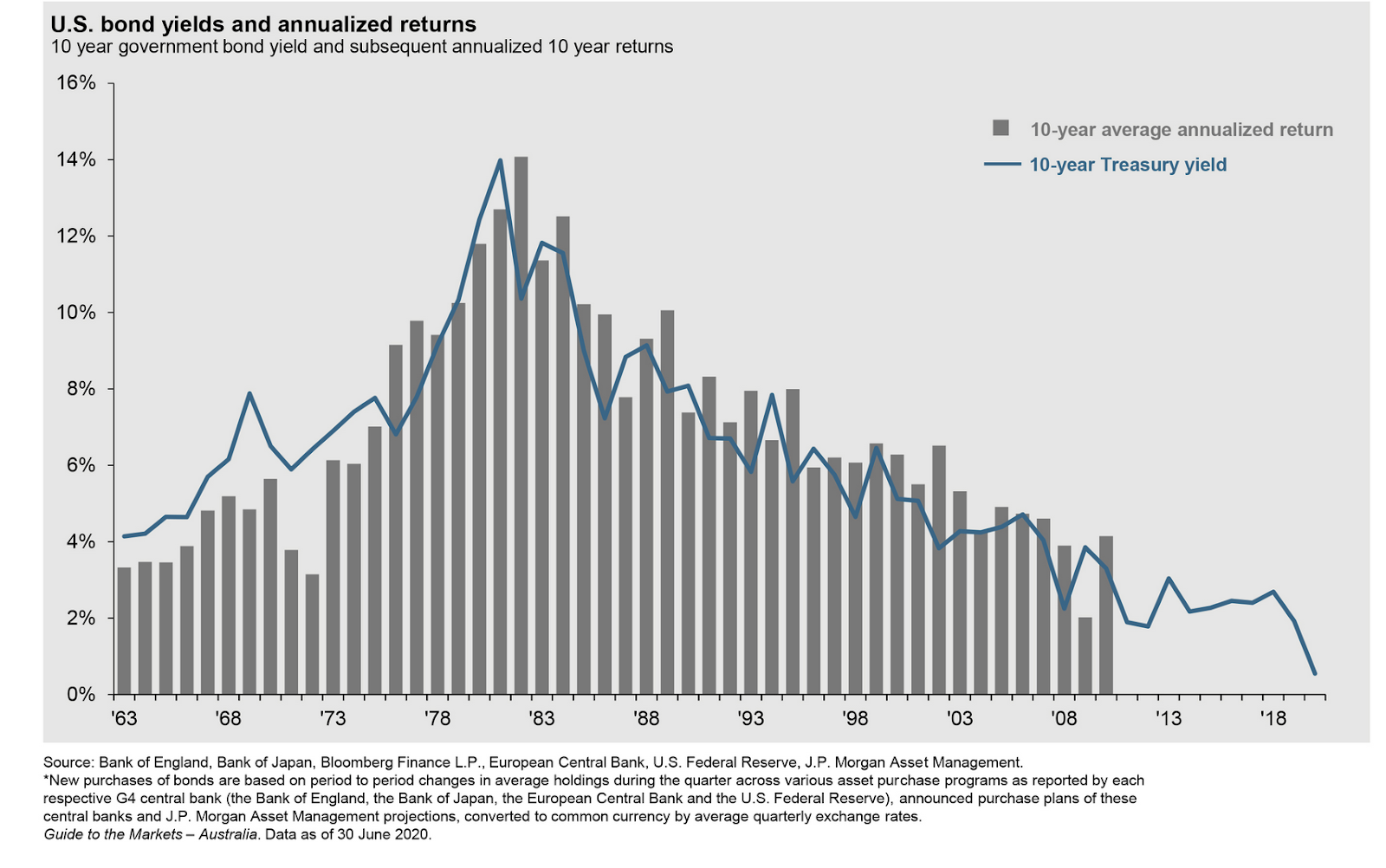

While bonds maintain their appeal as a safe haven investment, yields are so low that in many cases, they are below inflation. The yield on the 10-year US Treasury bond, the most watched government bond, is currently less than 1%. Nor are these low returns limited to the US: the Financial Times reported that as of June 2020, 86% of the global bond market yielded less than 2.0%.

As can be seen from the chart above, US Treasury yields have been on the decline for quite some time. The Fed’s decision means that ultra-low rates are here to stay for the foreseeable future.

Investors struggle to preserve capital while achieving returns

This ultra-low rate environment is extremely challenging for investors. Most investors would prefer to keep a portion of their portfolio low risk, fixed-income assets such as bonds, CDs or high-yield savings accounts. Allocating some of your portfolio to fixed income offers several benefits, including diversification, preservation of capital and passive income.

That being said, most investors also want this portion of their portfolio to earn a return, which is challenging with yields so low. As Shawn Khazzam, J.P. Morgan Asset Management’s head of alternatives solutions for the Asia-Pacific region, notes:

“In today’s ultra-low rate environment, the bond universe has changed significantly, with major investment implications for income investors… On an average annualized basis over the next 10 to 15 years, we expect only about 1% returns from traditional government bonds, posing a substantial challenge for income-oriented investors.”

With rates low for the foreseeable future, investors are faced with a difficult choice: do they forgo income for stability, or do they risk allocating more capital to riskier investments in order to achieve better returns?

Stock market valuations are high, but are they sustainable?

To many investors, low bond returns mean moving more money into equities. In contrast to anemic bond markets, US stocks have already recovered to their pre-pandemic levels. However, this has been combined with record levels of volatility. The VIX Volatility Index hit an all-time high in March, and while volatility has declined since then, the index has frequently surged above its long-term average levels. In addition, COVID-19 has radically impacted the volatility and likelihood of default of many sectors.

Some experts question whether the stock market is overvalued. David Rubenstein, co-founder of the Carlyle Group, told CNBC that “I think the market has somewhere more to go, but on the other hand, I don’t think it can keep going up forever at this pace.” Others believe that the market may be on the verge of a correction. Mike Wilson, Chief Investment Officer and Chief U.S. Equity Strategist for Morgan Stanley, recently suggested that we may soon experience another correction of up to 10%. A lack of confidence in current stock market levels isn’t limited to bankers and financial analysts — in August this year, 84% of Fortune 500 CFOs believed that the stock market was overvalued.

All this is to say that while it would be foolish to miss out on the current stock market rally, investors should also carefully consider their risk tolerance when allocating their portfolios.

Where can investors deploy capital?

With these considerations in mind, the question remains: how can investors allocate their portfolios to maintain diversification, ensure robust returns and preserve capital? Below are four investments that all offer better returns than bonds.

Preferred Stock

Preferred stock, or “prefs,” are a class of stock that offer investors many of the advantages of bonds with higher yields. Like bonds, prefs offer a fixed dividend specified as a percentage of the issuance price. This is in contrast to common stocks, where the dividend is periodically set by the company. If the issuer is unable to make the dividend payment, it can be suspended, although payments continue to accrue and are paid in arrears (unliked dividends on common stock). Prefs are typically less volatile than common stock and are uncorrelated with stocks or bonds, meaning they add diversification to a portfolio.

Gold

Gold is a popular alternative investment for investors in search of a hedge against inflation and/or a weak US dollar. Unlike owning a stock, gold is a real asset with intrinsic value. Recently, a bet on gold seems to have paid off for investors — the price of gold has increased nearly 600% since 2000. Gold is also uncorrelated with stocks, bonds and interest rate movements, making it useful for portfolio diversification. However, gold does have several disadvantages. It is not a source of passive income — investors only realize gains when they sell. Nor does gold have the upward potential of the stock market. Historically, returns on the S&P 500 have far exceeded returns on gold. Finally, the price of gold is volatile, which should give risk-averse investors pause.

Real Estate

Real estate is an alternative investment that will be familiar to most investors. Broadly speaking, real estate can be broken down into three main segments: residential, commercial and industrial. The pandemic had an immediate impact on real estate this spring, although some segments have since begun to recover. Many real estate investments offer a return through both periodic payments and price appreciation when the asset is sold. Real estate also offers portfolio diversification, although one disadvantage is that real estate investments are largely illiquid, meaning that converting them to cash is time consuming and/or entails significant transaction costs.

Farmland

Farmland is a class of alternative investments that is steadily increasing in popularity among investors. Relative to other alternative investments, farmland is a newer opportunity, not because it hasn't been around but rather because of high barriers to entry. With a boom in land ownership transfers expected over the next decade and the introduction of innovative investment platforms like FarmTogether, farmland investments are now available to accredited investors.

Over the past two decades, farmland has proven itself a strong adversary to the ever-growing gold market in the United States. With lower volatility and higher returns over the past few decades, farmland may just be replacing gold in many investors’ portfolios.

Like real estate, farmland offers investors a return through both periodic distributions and price appreciation. These returns are much more attractive than those currently offered by bonds: between 1998 and 2018, farmland returned an average of ~10%. Farmland is also an alternative to gold that offers a hedge against inflation with much lower volatility. Farmland is far and away one of the most inflation-proof investments around due to the perpetual need for farming in any economy - people need to eat, and this will never change. This makes farmland real estate particularly well-suited to retain value over time—even during recessions.

Finally, farmland is uncorrelated with public market securities like stocks and bonds, meaning that it adds significant diversify to a portfolio. Farmland’s scarcity value makes it an attractive option for those in search of a low-risk, high-returning investment.

Are you maximizing your returns? If your bond investments are underperforming, you might want to consider investing in farmland.

Click here to see farmland's historical performance, visit our FAQ to learn more about investing with FarmTogether, or get started today by visiting ways to invest.

Disclaimer: FarmTogether is not a registered broker-dealer, investment advisor or investment manager. FarmTogether does not provide tax, legal or investment advice. This material has been prepared for informational and educational purposes only. You should consult your own tax, legal and investment advisors before engaging in any transaction.

Was this article helpful?